Some of the main motivations behind adoption of the CBDC are that central banks, faced with dwindling usage of paper currency, seek to popularise a more acceptable electronic form of currency like in the case of Sweden…writes ANIMESH SINGH

The Reserve Bank of India (RBI) had, last week, announced that it will commence a pilot project of digital rupee (eRs) for specific use cases in the wholesale segment from November 1. The pilot project is for settlement of secondary market transactions in government securities.

Use of eRs-W is expected to make the inter-bank market more efficient. Settlement in central bank money would reduce transaction costs by pre-empting the need for settlement guarantee infrastructure or for collateral to mitigate settlement risk. Going forward, other wholesale transactions, and cross-border payments will be the focus of future pilots, based on the learnings from this pilot project.

The RBI had further announced that within a month of this pilot project, a similar project for the retail segment would also be launched in closed user groups comprising customers and merchants. Details regarding this would be made public soon, it had added.

All these preparations are in line with the announcement by Finance Minister Nirmala Sitharaman in her budget speech that the RBI will launch the central bank digital currency (CBDC) during the current financial year.

Let us therefore try and understand what exactly the CBDC or the digital rupee is.

The RBI defines the CBDC as the legal tender issued by a central bank in a digital form. It is the same as a sovereign currency and is exchangeable one-to-one at par with the fiat currency.

While money in digital form is predominant in India — for example in bank accounts recorded as book entries on commercial bank ledgers, the CBDC would differ from existing digital money available to the public because it would be a liability of the Reserve Bank, and not of a commercial bank.

Some of the key features of the CBDC would be that it will be a sovereign currency issued by central banks in alignment with their monetary policy, it will appear as a liability on the central bank’s balance sheet, it would be accepted as a medium of payment, legal tender, and a safe store of value by all citizens, enterprises, and government agencies.

In addition to this, the CBDC would be freely convertible against commercial bank money and cash. It would be a fungible legal tender for which holders need not have a bank account. Also it would be expected to lower the cost of issuance of money and transactions.

Some of the main motivations behind adoption of the CBDC are that central banks, faced with dwindling usage of paper currency, seek to popularise a more acceptable electronic form of currency like in the case of Sweden.

Also jurisdictions with significant physical cash usage seek to make issuance more efficient. Countries with geographical barriers restricting the physical movement of cash also had the motivation to go for the CBDC – for example, The Bahamas and the other Caribbean nations with small and large numbers of islands spread out.

Last but not the least, central banks seek to meet the public’s need for digital currencies, manifested in the increasing use of private virtual currencies, and thereby, avoid the more damaging consequences of such private currencies.

In addition to this, the CBDCs have some clear advantages over other digital payments systems, as it being a sovereign currency, ensures settlement finality and thus reduces settlement risk in the financial system. The CBDCs could also potentially enable a more real-time, cost-effective seamless integration of cross border payment systems.

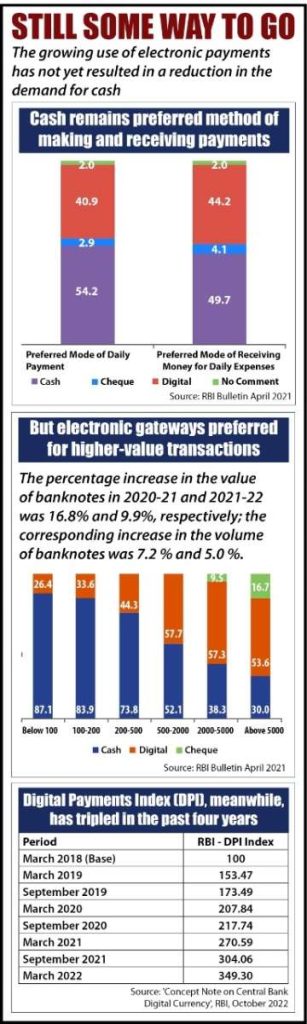

India has made impressive progress in innovation in digital payments. The payment systems are available 24×7, 365 days a year to both retail and wholesale customers, they are largely real-time, the cost of transaction is perhaps the lowest in the world, users have a wide array of options for doing transactions, and digital payments have grown at an impressive CAGR of 55 per cent over the last five years, a concept note by the RBI said.

Supported by the state-of-the-art payment systems of India that are affordable, accessible, convenient, efficient, safe and secure, the eRs system will bolster India’s digital economy, enhance financial inclusion, and make the monetary and payment systems more efficient. There are a large and diverse number of motivations for India to consider the CBDC, it said.